REITs that have been moving down the path of decarbonization and gathering information to assess climate-related portfolio risk have a running start to comply with potential changes ahead in the reporting and compliance landscape. Others that have been slow to start might need to scramble to catch up.

In March, the Securities and Exchange Commission (SEC) released its proposed Enhancement and Standardization of Climate-Related Disclosures for Investors. If finalized, it would become the first rule requiring all companies registered with the SEC to report, measure, and quantify material risks related to climate change in their registration statements and periodic filings.

Specifically, the rule addresses reporting on Scope 1, Scope 2, and Scope 3 emissions, as well as exposure to physical risks to assets and operations from climate-related events and transition risk related to compliance with federal, state, and local climate laws.

However, the final rule likely will be challenged in court as an overreach of the SEC’s regulatory authority and possibly on constitutional grounds, and it is quite possible that Congress might seek to change or overturn a final rule if Republicans win majorities of the House of Representatives and the Senate in the November elections.

“What the SEC has put forward sends a really strong message to companies about the importance of measurement, verification, and transparency around greenhouse gas emissions,” says Sarah King, senior vice president, sustainability at Kilroy Realty Corp. (NYSE: KRC). “For a long time we’ve thought that voluntary action from industry leaders will help solve the climate problem, and I think we can all agree that voluntary action alone won’t get society where we need to be fast enough. So, it is really impactful that the SEC has weighed in with such a comprehensive proposal,” she says.

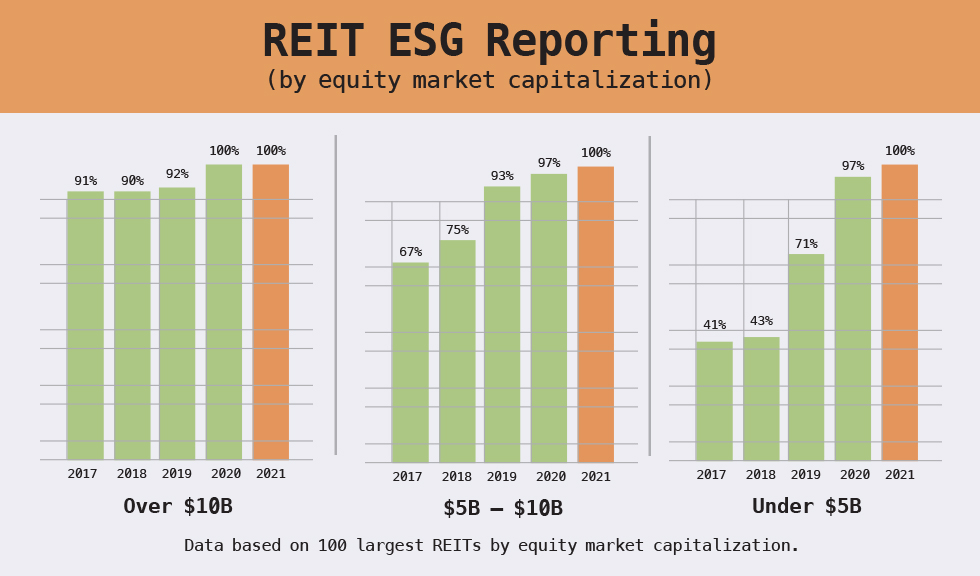

Lack of standardization has been a common frustration for both REITs and investors. In addition, voluntary sustainability and ESG reporting have become increasingly complex over the past decade with multiple disclosure and guidance frameworks such as CDP, GRESB, GRI, and the Task Force on Climate-related Financial Disclosures (TCFD). The various reporting platforms all request ESG data and narratives in slightly different ways. There also is room for interpretation from the investors and other stakeholders using the data from those frameworks to inform their decisions and engagement with companies, King notes.

Adapting to new SEC rules is rarely easy, and in this case, there are concerns about the resources companies will need to allocate in order to comply, with the heavy lifting ahead for some companies in a relatively short timeline. As currently written, compliance would start in 2024 (FY 2023) for the largest SEC registrants (market cap of $700 million or more), with a gradual phase-in for smaller companies.

REITs represent property sectors with different types of tenants, lease structures, and operating models, and not everyone has the same access to data, notes Fulya Kocak, LEED Fellow, senior vice president, ESG issues at Nareit. “The conversations that we’re having with REIT industry participants are around how can these disclosures be done in an effective way; how can challenges be handled; and how can we make it consistent based on all of these differentiating factors,” she says.

Unpacking the Proposed Rules

It remains to be seen what, if any, changes or modifications to the proposed SEC rules might occur following the public comment period, which closed on June 17. However, the REIT industry has been busy working to better understand details and developing strategies for compliance.

Indeed, on June 17 Nareit submitted comments to the SEC on the proposal, reflecting the key concerns of its members, noted Victoria Rostow, senior vice president & deputy general counsel at Nareit. She said that those concerns include the view that the proposal is a “highly prescriptive ‘one size-fits all’ approach” that would require REITs and other registrants to disclose information that could not be useful and/or could be confusing to their investors.

Rostow pointed out that other issues raised by Nareit include the need for increased liability protections, the need for more flexible timing and better mechanics for reporting, the need to lower the cost and burdens of compliance, and the desire for extended phase-in periods.

Nareit is also requesting that Scope 3 disclosures be voluntary, while reiterating its long-standing view that REITs and other landlords should only be required to report on climate data arising from operations under their direct and immediate control and that REITs and other landlords should not be required, as a default, to report on their tenants’ emissions.

If the proposed rules around Scope 3 reporting move forward in their present form, there will need to be more conversations around how Scope 3 is defined and how data is accessed, Kocak adds. For example, there are bigger barriers to data acquisition with respect to assets with long-term triple net lease structures. “Because that data is not always easily accessible, or may not be accessible at all, there will have to be a lot of engagement with tenants,” she says. Introducing green leases is a solution, but some assets have long-term existing leases in place that will take time to transition.

A second issue is how to report on physical and transition risk when the methodologies for doing so are not standardized, while a third issue centers around the timing of reporting.

Typically, financials come out before most companies finish finalizing climate-related data for the year. As currently written, the SEC would require “limited assurance” on Scope 1 and 2 emissions in the first two years of compliance and then “reasonable assurance” thereafter. Some companies are wary that there isn’t sufficient time to both collect the data and complete the third-party assurance process so that the data can be included within the 10-K document. Most REITs are reporting on dozens, if not hundreds, of assets. So, it is a large undertaking to manage all of that data, and there can also be a lag in collecting data, King notes.

A fourth issue is how to encourage the use of standardized tools, such as the EPA’s EnergyStar Portfolio Manager and Green Button, and whether using those tools could get some sort of benefit or safe harbor.

“For the industry, two key challenges to standardized ESG reporting include Scope 3 data availability and the need for context across key metrics. We support efforts that improve the rigor of ESG reporting and provide quality and comparable data to investors and other stakeholders, complemented with industry and company-specific context,” says Suzanne Fallender, vice president, global ESG at Prologis, Inc. (NYSE: PLD).

Prologis has a long-standing commitment to ESG and has been reporting on its ESG performance for more than a decade, including its Scope 1, 2, and 3 emissions. “We are committed to providing data that is in context, useful and actionable. This meets the data needs of not only our investors, but also those of our customers as we help them advance their own ESG goals and decarbonization strategies,” she says.